From EMI to Empowerment: Rethinking Rural Lending for Farmers and Nano Entrepreneurs

Kumar Abhishek #FinancialInclusion #RuralCredit #MicroEntrepreneurs

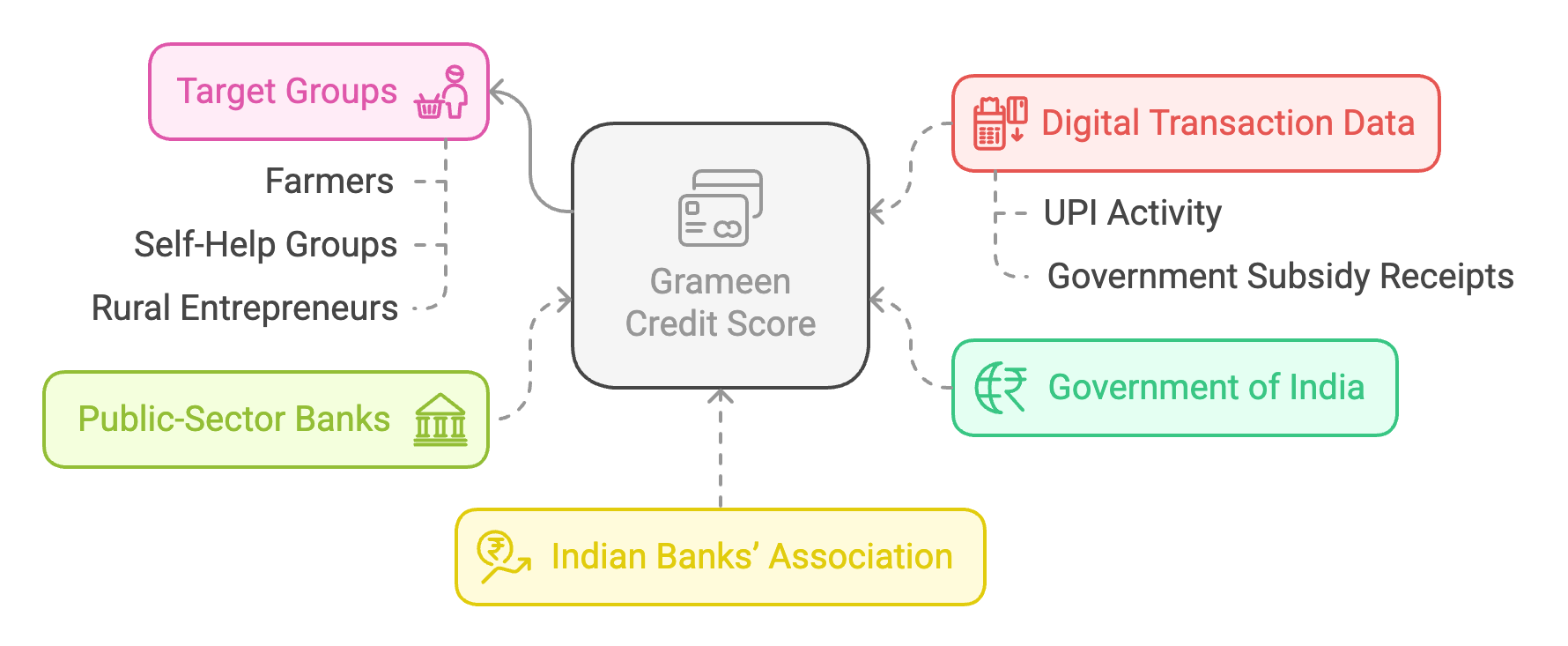

First and foremost, a warm thanks to the Government of India, the public-sector banks, and the Indian Banks’ Association (IBA) for spearheading the forthcoming “Grameen Credit Score” system, as reported in the Mint. This initiative marks a critical step toward bridging India’s rural credit gap and fostering financial inclusion for farmers, self-help groups (SHGs), and rural entrepreneurs.

According to the Mint article, the proposed Grameen Credit Score is intended to enhance formal lending to the traditionally underserved—farmers, self-employed individuals, SHGs, and more. By harnessing digital transaction data (including UPI activity and government subsidy receipts), the framework aims to provide robust, data-driven insights into creditworthiness.

The Urgent Need for Structured Credit Scoring §

This shift toward more precise credit risk assessment is long overdue. As per various surveys by the Reserve Bank of India (RBI) and industry bodies, about 70% of small and marginal farmers still rely on informal sources of lending, such as local moneylenders, due to a lack of formal credit history. A structured credit scoring system can potentially unlock enormous lending capacity, channeling funds directly to where they are most needed.

Inclusivity Beyond Farmers §

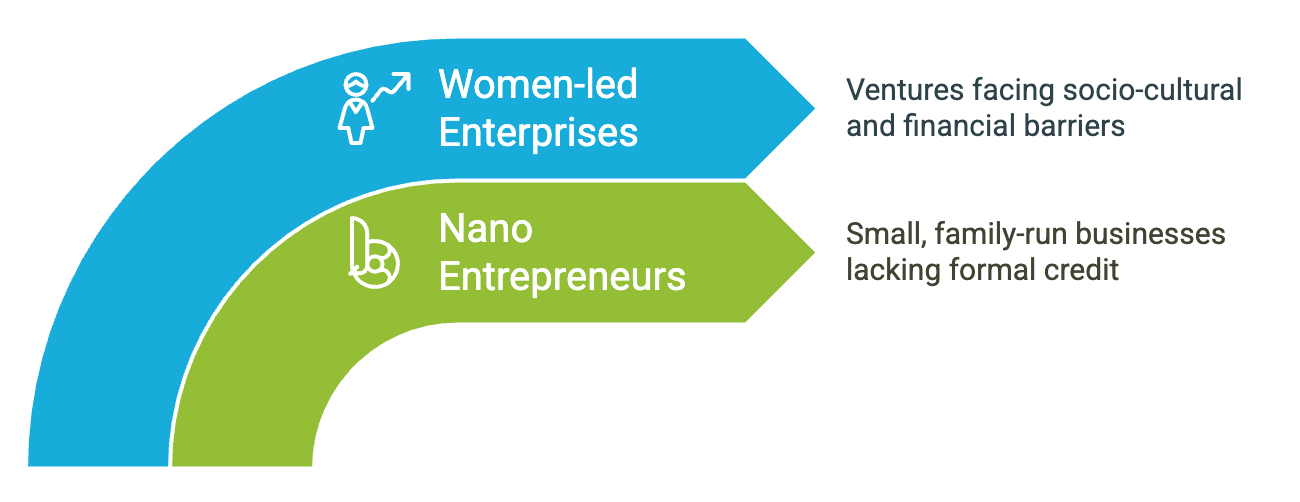

While farmers certainly form the backbone of rural India, it is vital to include nano entrepreneurs, especially those who employ fewer than five people (sometimes just the family itself), and women-led enterprises. This broader lens ensures that all micro and nano enterprises—often the most vulnerable—can also benefit from the proposed Grameen Credit Score system.

- Nano Entrepreneurs: Typically small or family-run with fewer than five employees, often lacking formal credit footprints.

- Women-led Businesses: Facing unique challenges — such as limited access to financing and socio-cultural barriers — these ventures can greatly benefit from targeted credit products.

The Mint piece highlights how digital footprints will be considered, but this emphasis should be expanded to ensure every nano and micro venture is included, bolstering inclusive growth for the entire rural economy.

- Scale of Micro-Enterprises: According to the Ministry of Micro, Small & Medium Enterprises (MSME), micro enterprises constitute over 99% of all MSMEs, with a significant fraction employing fewer than five people.

- Women’s Participation: Data from the Sixth Economic Census indicates that over 13% of Indian establishments are owned by women entrepreneurs, many of whom operate at the nano or micro scale. With targeted credit scoring and relevant products, this figure could climb, propelling female entrepreneurship in rural areas.

Challenges of EMI-Centric Lending for Rural India §

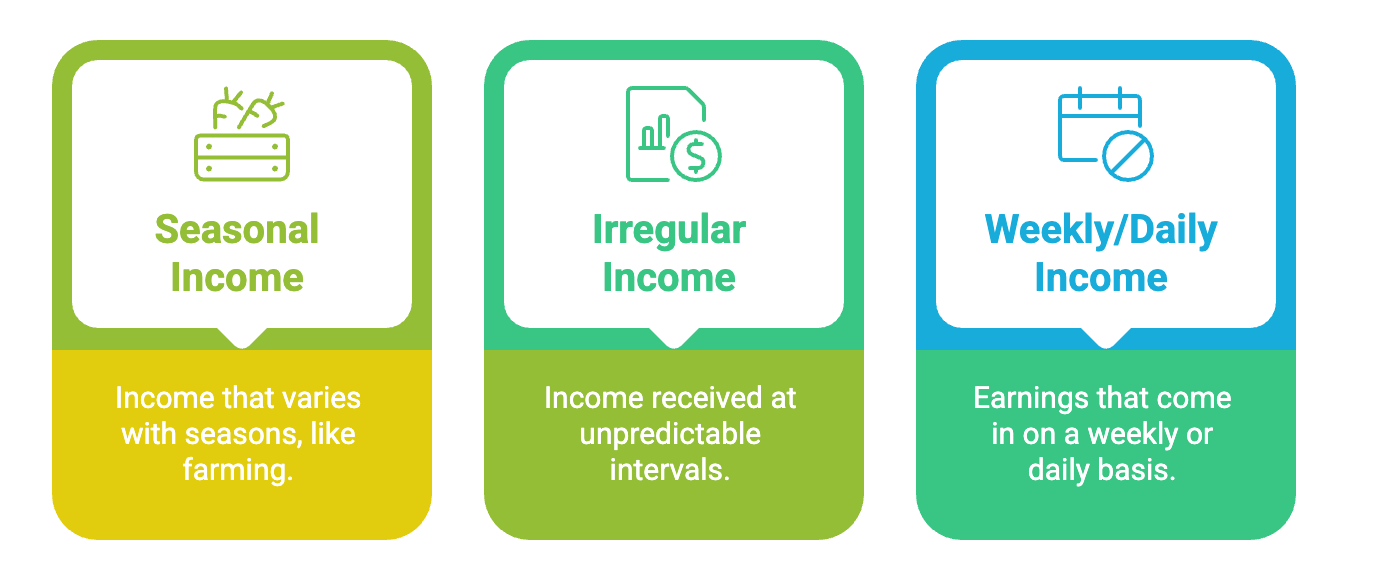

India’s standard credit products — from personal loans to credit cards — are heavily skewed toward an EMI model, primarily designed for salaried individuals with predictable monthly paychecks. This approach often becomes problematic for those whose incomes are:

- Seasonal (e.g., farmers who earn post-harvest),

- Weekly or daily (shopkeepers, agricultural laborers, nano entrepreneurs),

- Irregular (small businesses that receive lump-sum payments at irregular intervals).

For instance, a small kirana store owner might see most of their income around festive seasons and very little during off-peak months, making strict EMI deadlines particularly difficult to manage.

To achieve the mission of “Viksit Bharat,” credit solutions must evolve beyond the EMI-based structure. Even credit cards, which offer a ~45-day grace period, presuppose monthly salary inflows — an assumption that often does not hold true for entrepreneurs with variable cash flows.

Rethinking the Lending Model §

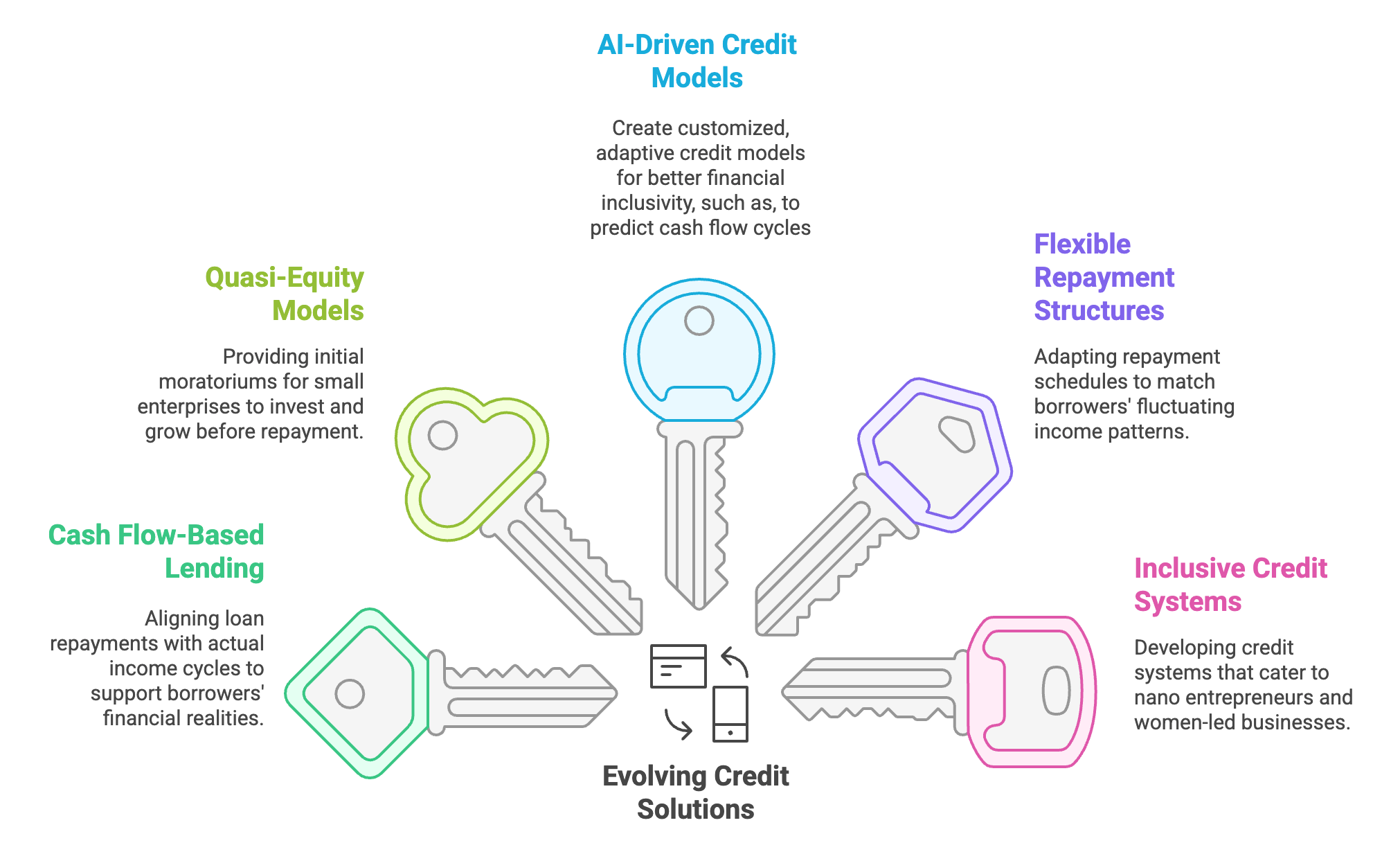

The Mint story highlights the government’s intent to use digital footprints for better credit decisions, but this should also be a cue to embrace flexible repayment structures and innovative loan products. For instance, daily, weekly, or seasonal repayment schedules can be more appropriate for borrowers with fluctuating incomes. By matching repayments to real cash inflows, lending can become truly dynamic and responsive.

- Cash Flow–Based Lending: Instead of insisting on a strict EMI schedule, loan repayments could align with actual inflows. A farmer might repay a higher chunk right after a bountiful harvest, then pay little to none in low-earning months.

- Quasi-Equity or Micro-Equity: Many tiny enterprises require an initial moratorium before repayment starts—akin to equity financing—so they can invest, scale, and generate stable revenue. Such structures are key to sustainable long-term growth and are especially relevant to rural entrepreneurs.

Leveraging AI for Rural Credit §

India’s rapid strides in digital infrastructure and AI-driven solutions open up a golden opportunity. Large Language Models (LLMs) and “Generative AI” can analyze disparate data points to create customized credit models specifically designed for rural entrepreneurs. Some key benefits include:

- Predicting cash flow cycles more accurately, factoring in seasonal or irregular income

- Automating repayment schedules based on real-time data

- Mitigating risk through constant monitoring

- Adaptive lending limits that adjust to changing cash flows

An open-source foundational model specifically tuned to these rural contexts could revolutionize credit delivery. It would help banks, NBFCs, and microfinance institutions scale effectively while keeping default risks in check.

Expanding the Vision: Beyond EMI §

The upcoming Grameen Credit Score, as reported in Mint, is a welcome development — one that could serve as a cornerstone for more inclusive credit systems across India. However, it must be broadened to cover nano entrepreneurs and women-led businesses comprehensively. Designers of new lending products should also move away from standard EMI timelines to truly accommodate the diverse income patterns that characterize rural India.

By introducing more flexible credit products and harnessing the power of AI-driven tools, we can build an ecosystem that not only aids farmers and SHGs but also catalyzes the growth of micro and nano enterprises. Ultimately, this will drive the kind of sustainable, inclusive growth that the nation envisions under the banner of “Viksit Bharat.”

Cited Article: “Govt to roll out credit rating for rural borrowers in six months,” Subhash Narayan & Rhik Kundu, Mint, February 19, 2025.

Disclaimer: Data points cited on MSMEs, micro enterprises, and women-owned establishments are based on publicly available information from sources like the RBI, the Ministry of MSME, and the Sixth Economic Census.

All Posts